While study Inventory methods On the one hand, inventory management decisions are not very dramatic, and on the other, they determine how you make profits, taxes, and cash flows.

A very neglected decision that business owners engage in is the choice of inventory methods of FIFO or LIFO. Both appear to be mere accounting principles on paper. The truth is that the decision to use the wrong inventory technique will misrepresent your profit statements, over-value your tax due and give you an incorrect pricing strategy.

I have witnessed businesses expanding in terms of sales and not being able to rest on cash since their inventory valuation was not that of reality. When you have to work with stock, be it selling the products, producing the goods, or trading commodities, it is not a free choice whether to know about FIFO vs LIFO. It is a tactical move that immediately determines the state of the health of your business.

What Is FIFO?

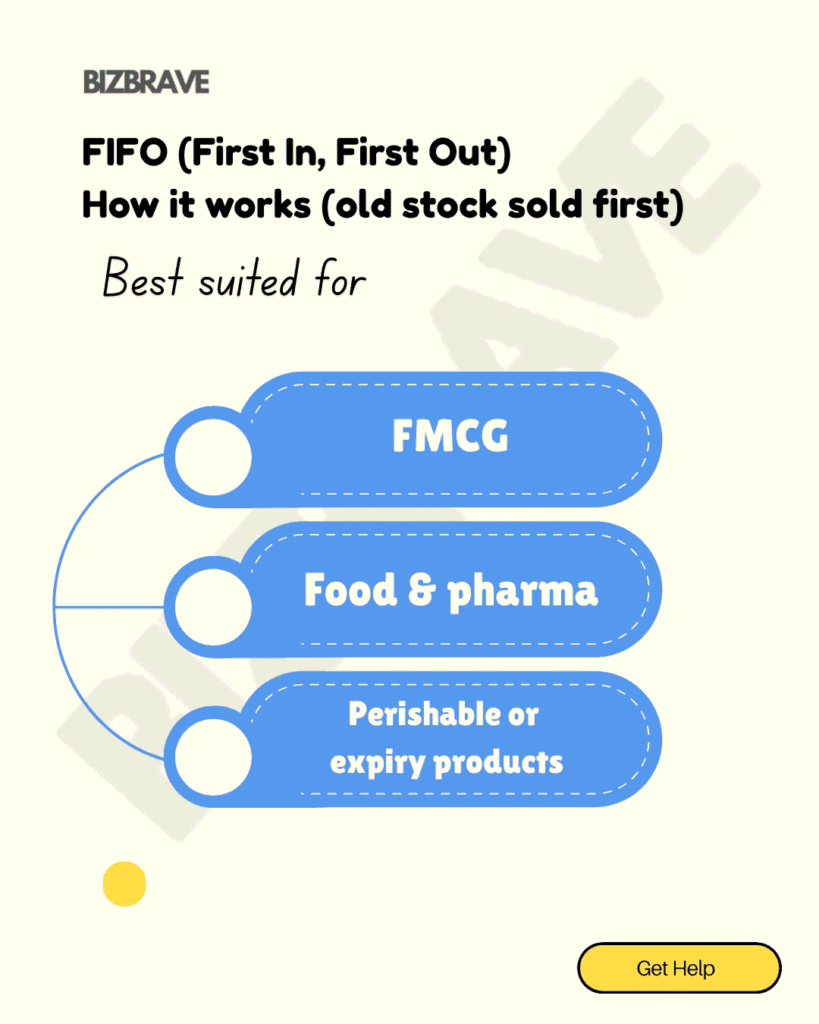

FIFO or First In First Out is an inventory accounting technique in which the cost of oldest purchased or produced goods is charged at the moment it is sold in the first stage, with the newest inventory kept in the stock.

FIFO in a very basic definition presupposes that the very first thing you purchase or produce is also sold first, regardless of the physical locations of the items. This mode is very similar to the business practices in the real world, particularly of products that have a short shelf life, a high turn over or whose trends keep on changing.

What Is FIFO?

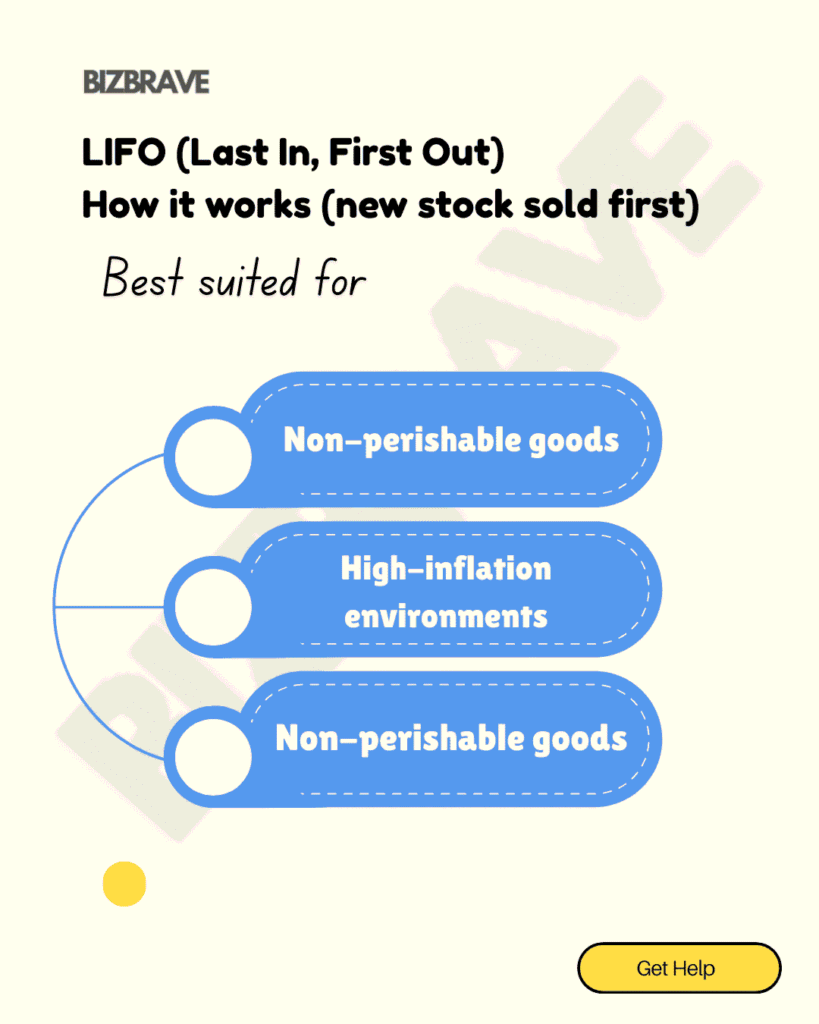

LIFO also known as Last In First Out, is an accounting approach of inventory accounting in which the cost of last purchased or produced goods is noted as sold first with the old inventory costs kept in stock. This implies that the current sales are contrasted with the latest costs which can decrease the reported profits at the times of increasing prices and allow to control a tax liability at available opportunities.

The LIFO method is primarily applied in price volatile goods or bulk goods based industries, and fails to represent the flow of goods in reality, and tends to under-value the closing inventory.

The Hidden Inventory Issue that most of the businesses pay no attention to(FIFO vs LIFO).

Majority of business owners are concerned with sales, marketing, and operations. The accounting of inventory is normally only given attention when audits, GST or stock mismatches are observed. That is the point where it begins to go wrong.

Frequently, it is not a sales problem, but the cost recording of inventory. Your inventory approach determines which cost is going to be reflected in your profit and loss statement when purchase prices vary. Unless you are mindful of whether to use FIFO or LIFO, then your financial statements are probably providing you with half-truths.

This gap increases as the businesses expand. Manual tracking, assumptions and outdated methods can work on small scale, but silently fail once volumes, suppliers and SKUs grow.

Reality Check: FIFO and LIFO Do Not Move Your Stock: FIFO vs LIFO Move Your Numbers.

We should get out of a great fallacy. FIFO and LIFO do not determine whether a certain physical product becomes the first to leave your warehouse. They merely make a decision on what cost is carried to be sold.

FIFO (First In, First Out) presupposes to sell the oldest inventory first. LIFO (Last In, First out) works on the assumption that the latest inventory is sold out first. The impact of this difference on the three areas of importance directly are Cost of Goods Sold (COGS), closing stock value and taxable profit.

It is the right decision based on the industry you are in, inflation direction, regulatory regulations and long-term business perspective.Companies that consider inventory accounting as a commodity accountancy overlook its strategic importance.

The Concept of FIFO Understanding: When Simplicity and Reality Agree.

The most popular inventory system all over the world is FIFO. Under the FIFO, your oldest stock would be used as sold first, and newer inventories are held in closing inventory.

Physical stock movement is inherently reflected by FIFO when the goods of the business are perishable, expiry sensitive or fast moving consumer goods. It eliminates the stagnant stocks lying around and offers the inventory value a closer estimation.

Financially, FIFO tends to record greater profitability in a period of inflation due to the match of old and low costs with the current selling prices.

The reason why many business owners are fond of FIFO is it is simpler to comprehend, simpler to explain to auditors, and is widely accepted by accounting standards in most nations such as India.

However, FIFO is not perfect. In times of cost inflation, reported strength may not be cash strong. Later many businesses that fail to plan this tax tend to have pressure.

LIFO: Knowledge of LIFO as a Strategic butlimited Practice.

LIFO operates just the reverse. It presupposes that the last bought inventory is sold, and old items remain in the records of the inventory.

Cost matching is the major attraction to LIFO. Newer costs are more expensive during inflation and thus the profits are seen to be low enough to pay lower taxes.This will help in sustaining cash flow in certain scenarios particularly in business involving commodities or goods exhibiting price volatility.

Nonetheless, there are significant limitations of LIFO. It is prohibited in a lot of accounting regulations, such as the Indian accounting and IFRS. It may severely understate closing stock on the balance sheet even where permitted, providing an untrue idea of the health in business. In the long run, the inventory records could consist of very old costs which are no longer reflective of the reality.

This is why LIFO, though appealing in theory, will be impractical to most businesses.

FIFO vs LIFO: Which Businesses need to select what?

There is no question of what appears better on the paper, FIFO or LIFO. It is a matter of being on par with the way your business works.

FIFO is mostly more appropriate in enterprises that handle perishables, retail products, FMCG, pharmaceutical products, and electronic products, as well as on any business where the freshness of stock is important. It brings out transparency, conformity, and purer financial statements.

LIFO, when legalized, can be advantageous to businesses that deal in large quantities of commodities or materials whose prices are often likely to fluctuate and where tax efficiency is of major priority.

The actual error made by the businesses is adopting an approach and never coming back to it. Markets change. Inflation changes. Your business scale changes. The inventory practices need to change.

A Personal observation of working in the growing businesses.

One pattern that I have observed over the years is the following. It is not a misfortune to businesses that they either use FIFO or LIFO, it is that they have not investigated the effect of their decision(FIFO vs LIFO).

Most of the expanding businesses are still maintaining manual inventory records or being on simple spreadsheets not knowing the impact of inventory appraisal on the pricing, profit and cash planning. As companies spread in various locations or mediums, there is a rise in the complexity of inventory and a multiplication of incorrect assumptions.

Inventory accounting must not baffle the business, but help business decisions.When your methods of inventory correspond with your operations and financial objectives, then your reports become instruments–not paperwork.

Takeaways: The key to the correct inventory method FIFO vs LIFO.

The initial process is to know your nature of products. When you have goods that are of a perishable nature, degradable or those whose lifespan is very short, then FIFO is often the best, and more practical choice.

The fact that inventory accounting is matched with physical flow helps to minimize the errors and surprises. Second, have your inventory procedure on a yearly basis. A strategy that proved effective in a low price environment can damage profitability in a high price market.

Just as in pricing strategy, inventory strategy needs to be reviewed. Third, you should not use manual inventory tracking as your business expands. The mistakes do not manifest themselves in the short term, but they accumulate. Lack of consistency in data will cause erroneous judgments particularly in pricing and buying.

When your cost information is either obsolete or misleading, then the sale price will appear profitable when it is really decreasing margins.

Lastly, the last thing to remember is never change inventory methods without knowing about tax and compliance. Even a minor accounting modification may present a long-term reporting and audit problem unless planned adequately.

Why Inventory Method is a Strategic Choice and not an Accounting Process.

Inventory is in the crossroad between operations, finance, and strategy.

Under conditions that inventory valuation corresponds to business reality, decision-making will be more apparent: buying to pricing to expansion.

Good companies do not sell more. They know their figures very well. When properly implemented, inventory accounting turns into a mute strength.

Frequently Asked Questions (FAQs)

How does FIFO and LIFO differ as methods of inventory?

The primary difference is in the recording of the inventory costs. FIFO presumes that the stock is sold out in terms of its age with the oldest being sold first and LIFO presumes that the stock is sold out in terms of its age with the latest one being sold first. This has an impact on profit, taxes and valuation of inventory- but not the actual motion of stock.

Is LIFO allowed in India?

No. LIFO is not allowed under both Indian accounting standards and IFRS. FIFO and weighted average compliance and reporting are common in most Indian businesses.

What inventory method will lower the tax liability?

In the case of inflation, LIFO may decrease the taxable profit since the costs that were incurred in the recent years can be balanced against sales. LIFO however is limited in most parts so FIFO is the best to use by most businesses.

Is it possible to alter inventory approach later in a business?

Altering inventory practices affects financial statements, tax statements and compliance. Vocational advice is highly encouraged prior to a change.

Is FIFO superior to small businesses?

In most cases, yes. FIFO is simpler to comprehend, generally embraced and consistent with actual stock flow. It offers a cleaner reporting of finances and reduced compliance issues in the growing businesses.

Final Thought

Inventory amount of money on shelves.The way you quantify it determines the prudence of your progress. FIFO or LIFO does not deal with the preference of accounting- it is about business clarity.When the inventory approach that you use justifies the reality, your judgments are more effective, less complicated and more assured.